– Hello. I’d like to introduce you to a revolutionary program that since 2004 has helped thousands of homeowners all across America get ahead financially and on track to save millions of dollars in interest payments on their mortgages and other debts. And as a result, eligible homeowners are now able to pay their 30-year mortgages off in as little as five to seven years, all without changing their current lifestyle and without any refinancing required. Paying off your mortgage is a lot like taking a road trip. However, instead of you choosing the route, the bank hands you a map with each and every turn they want you to take.

It’s an exact schedule of payments every month for 30 years and the bank’s schedule is not the fastest route. In fact, their schedule zigzags and goes on and on for miles of unnecessary distance. Are there better routes? Absolutely. The closest distance between two points is a straight line, correct?

Well, this program shows you the straight line and how eligible homeowners can fly through their mortgage in as little as five to seven years.

How does this program get you paid off so fast? Before I share the secret, I want you to understand that banks are very good at building wealth with your money. As an important part of their wealth-building strategy, the banking industry has taught us to keep our money separate. What do I mean by separate?

Well, we are taught to set up our checking and/or savings account and deposit our money over here. And we’re taught to take out our loans and make payments to those loans separately over there, never combining our positive cash accounts with our interest-charging loan accounts.

But who benefits from this separate account structure more, you or the banks? To understand why we are taught to manage our finances separately like this, we need to understand some basic principles of banking and money, and how it works. Each time we deposit and hold money in our checking and/or savings accounts, also known as deposit accounts, the lender makes money off of interest by lending our money out in the form of loans to borrowers.

And each time we take out a loan, the lender again makes money each time we pay them an interest payment.

So let’s go over a couple quick examples of how our money helps the lending industry build wealth. Let’s say, based on the money account holders like you and me have deposited in our checking and savings accounts, the bank lends out $5,000 to other borrowers in the form of credit cards. And while we earn close to zero interest on our money, the lender earns around 18% interest on those credit cards. That means that the lender was able to earn roughly $900 in interest annually based on our money while we earned close to zero.

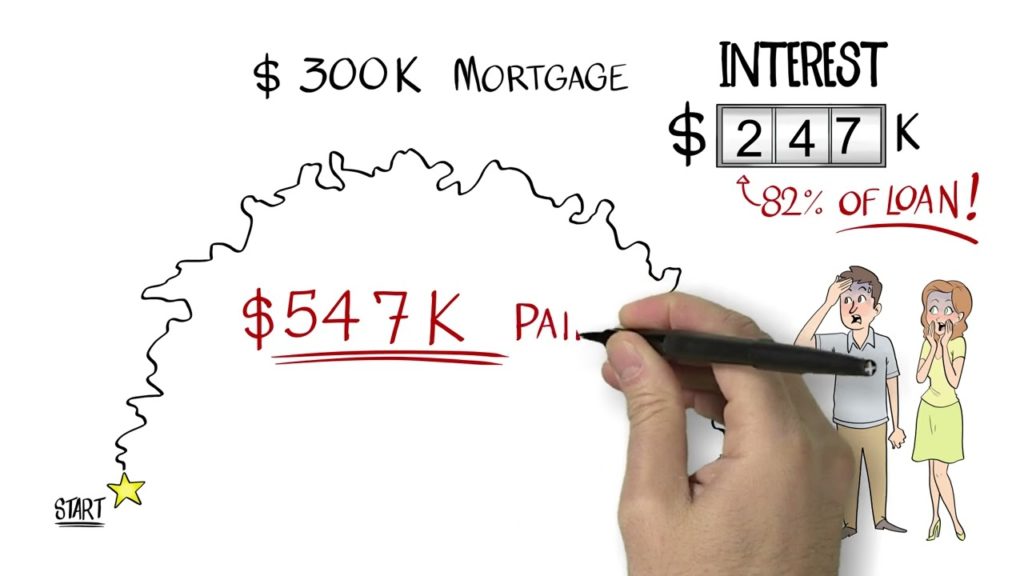

As another example, let’s say we take out a 30-year $300,000 mortgage at 4.5%. 4.5% doesn’t seem like it would add up to much, does it? But over this 30-year mortgage, we would pay over $247,000 just in interest payments.

That’s actually over 82% of the original loan amount you borrowed just in interest. Quite a far cry from the seemingly reasonable 4.5% rate, right? By following this simple concept of holding billions of dollars worth of banking clients money on one side and then lending our money back to us with interest on the other, the lending industry is able to build tremendous wealth.

Now think about this.

With all things being equal, the more money we owe, the more interest they collect and the less money we owe, the less interest they collect. So, if banks make more money based on the total amount we owe, there’s one guaranteed way to reduce the total amount we owe immediately. What if, instead of following the bank’s map of keeping your account separate, you could actually transfer or merge the money in your deposit accounts against your loan accounts, literally decreasing the total amount owed immediately? By doing this, it would instantly bring down the amount you owe and thus, reduce the amount of time and interest the bank has you scheduled to pay. Again, the less money you owe on your debts, the less interest you will pay, right?

With that being said, we would now like to introduce you to the Money Max Account.

The Money Max Account is a smart online financial system, programmed with extremely effective debt elimination strategies. The Money Max Account utilizes a standard checking and savings account and strategic financial algorithms to help drive its debt elimination strategies. With these financial algorithms, the system is programmed to constantly analyze and identify the most strategic debts to eliminate in the most beneficial order and timing. The system monitors your finances 24/7 and constantly calculates the specific timing and amounts of money to transfer from your checking and/or savings accounts to strategically reduce each of your loan balances, thus lowering the balance in which interest accrues and canceling an optimum amount of time and interest charges on your loans.

The debt elimination system is specifically programmed to help eliminate all of your debt, including up to a 30-year mortgage in as little as five to seven years, while saving tens to hundreds of thousands of dollars in interest without requiring you to change any of your current budgets.

The Money Max Account is like having 100 accountants working 24/7, calculating and strategizing the exact timing, amount, and frequency of each transfer in order to achieve some of the greatest time and interest savings imaginable. And it’s as easy to use as point and click. As you can see, you are now canceling out an optimum amount of time and interest charges with each and every step you take. And by continuing to follow the program’s cycle of strategic transfers and deposits, you literally change your mortgage schedule, effectively canceling out tens to hundreds of thousands of dollars in scheduled interest charges and accelerate the payoff of your mortgage and other debts to a fraction of their regular time.

(distant cheering) Now, do you remember our $300,000 mortgage example, the mortgage that would normally charge over $247,000 in interest charges over 30 years? By using our online financial acceleration system, this same mortgage could now be 100% paid off in as little as five to seven years, paying as little as $68,000 in interest charges versus $247,000 in interest.

That’s a savings of up to $179,000 in interest and up to 25 years worth of canceled mortgage payments. And again, the Money Max Account doesn’t just work on mortgages. It also strategically identifies the fastest way to accelerate the payoff of all of your debts.

We know that you and your family are unique and no two homeowners finances are the same. In just a few minutes, the Money Max Account can tell you how much time and money you can save.

Maybe your payoff is 10 plus years, maybe it’s seven, or maybe it’s five. What’s your debt-free number? What could you do with up to 23 to 25 years worth of mortgage payments back in your pocket?

Imagine now being able to invest that money and earn interest instead of just handing it over to the bank. It’s things like this that change our financial future and puts a big smile on people’s faces. Of course, you can see why the creators of this award-winning program have been featured in magazines such as Broker Banker, Real Estate Investor, and Success From Home magazine. They’ve also won the Ernst and Young Entrepreneur of the Year Award in the financial services category. Be sure to get back with a representative who sent you this video and ask them to run a free savings report that will show you just how much time and money this program could save you.

What’s your debt-free number? (lighthearted music).

Read More: Rosacea: Erkennen der Symptome und Auslöser sowie wichtige Tipps zur richtigen Behandlung

{kind=link}